The Bitcoin Accounting Edition

On market making, revenue, and GAAP

Guan Yang (GY) is a data scientist based in New York, sometimes working on financial data, and a big fan of Cash App and its boosts.

Guan here. Look up the financial statements for Square, Twitter founder Jack Dorsey’sother company which is probably best known for its Cash App, and you’ll see $4.6 billion in “Bitcoin revenue” in 2020, which is almost half the company’s total revenue. Cash App provides a debit card with popular “boosts”, and has also added the ability to trade stocks and Bitcoin, which is where all that revenue comes from.

Open the Cash App and buy a small amount of Bitcoin—it lets you purchase as little as $1 worth—and Jack doesn’t go out and find someone you can trade with. Instead, you’re buying Bitcoin directly from Square, the same way you might buy gold from a dealer with a storefront. A few seconds or minutes or hours later, someone else wants to sell their Bitcoin at a slightly lower price, and Jack buys it (as far as I can tell from reading the 10-K), making a modest profit facilitating those trades as a market maker, acting as the counterparty for every Bitcoin trade in the app.

If Cash App users are net buyers or sellers over a period of time, Jack then goes out to the wholesale market and buys or sells larger amounts of Bitcoin (and not $1 at a time), so his stockpile of Bitcoin roughly matches the Bitcoin balances in Cash App accounts. But Square’s accountants count all the money Cash App users spent buying Bitcoin as revenue, and in 2020 those users bought $4.6 billion worth of Bitcoin. That sounds like a lot, but the corresponding cost is $4.5 billion, so Jack’s profit on all that trading netted out at $97 million.

Coinbase, another big cryptocurrency company, which just filed for an IPO today, is also a market maker, but not to nearly the same extent as Jack. Instead Coinbase’s customers tend to trade directly with each other on the company’s platform. So even though there they facilitated $193 billion in transactions in 2020, total revenue is lower, at only $1.3 billion.

When your business is buying and selling the same stuff all day long, doing the accounting this way greatly exaggerates how much business you have. And it’s not how the accounting works for Square’s other lines of business. The second-largest of those, by “revenue,” is processing credit card payments through those sleek black terminals now seen in every hipster coffee shop. Jack processed payments of $103.7 billion through those terminals in 2020, and charged the stores $3.3 billion in fees. But only the $3.3 billion counts as revenue, not the full $103.7 billion people spent on lattes.

Real images from @cashapp on Instagram

Counting all the customers’ asset purchases as revenue is also not how it’s done for other financial companies. For a bank such as Bank of America, which tends to receive a lot of interest and also pay out a lot of interest, “revenue” is net interest income, the difference between interest received and interest paid out, plus things like overdraft fees. (This means that if something goes terribly wrong, a bank can have negative revenue.) Bank of America is also a market maker through its securities division, and only reports the profit from market making as revenue, $8.4 billion in 2020. Virtu, a major market maker in the stock market (and one of the five used by Robinhood), also only reports its $2.5 billion net trading income as revenue. Not the full value of the stocks it sold over the course of last year, a sum which is orders of magnitude larger.

Why is this interesting?

Accounting is supposed to summarize the complexities of a company, making the same concepts comparable across different companies and over time. An investor who spent some time with Square’s financial statements would quickly understand what’s going on. But lots of traders don’t even look at the reports directly, but instead use a stock screener tool, or more sophisticated quantitative models, and never appreciate the weird way Square’s revenue is recognized.

The numbers in Square’s annual report feed into the databases of commercial vendors such as Bloomberg and Refinitiv, which in turn feed into a whole ecosystem of retail and professional investment tools. Refinitiv’s database has a line for net sales of $9.5 billion, which includes the full value of all the Bitcoins bought by Cash App users along with the rest of the revenue Square took in for the year, and that $9.5 billion number feeds into all the companies that use Refinitiv data. That same ecosystem will see $3.2 billion for Virtu Financial in the net sales column, and treat it as the same data type as Square’s net sales, even though, as we saw, they’re quite different.

As far as I know, Jack’s finance team isn’t doing anything wrong here, and is following all the relevant accounting rules. Whoever came up with the accounting rules probably thinks all this is totally reasonable and finds it puzzling that anyone could find it interesting. But this is what you’re dealing with if you use financial datasets. And the lessons here will apply more widely to almost any use of “data.”

As a US company, Square follows what are quaintly known as GAAP, or “Generally Accepted Accounting Principles.” GAAP is intended to be a common reporting standard, so anyone who knows GAAP should be able to read and understand financial reports for any company. But it still leaves a lot up to interpretation, and in the end it’s very hard to compare companies in an apples-to-apples way. (GY)

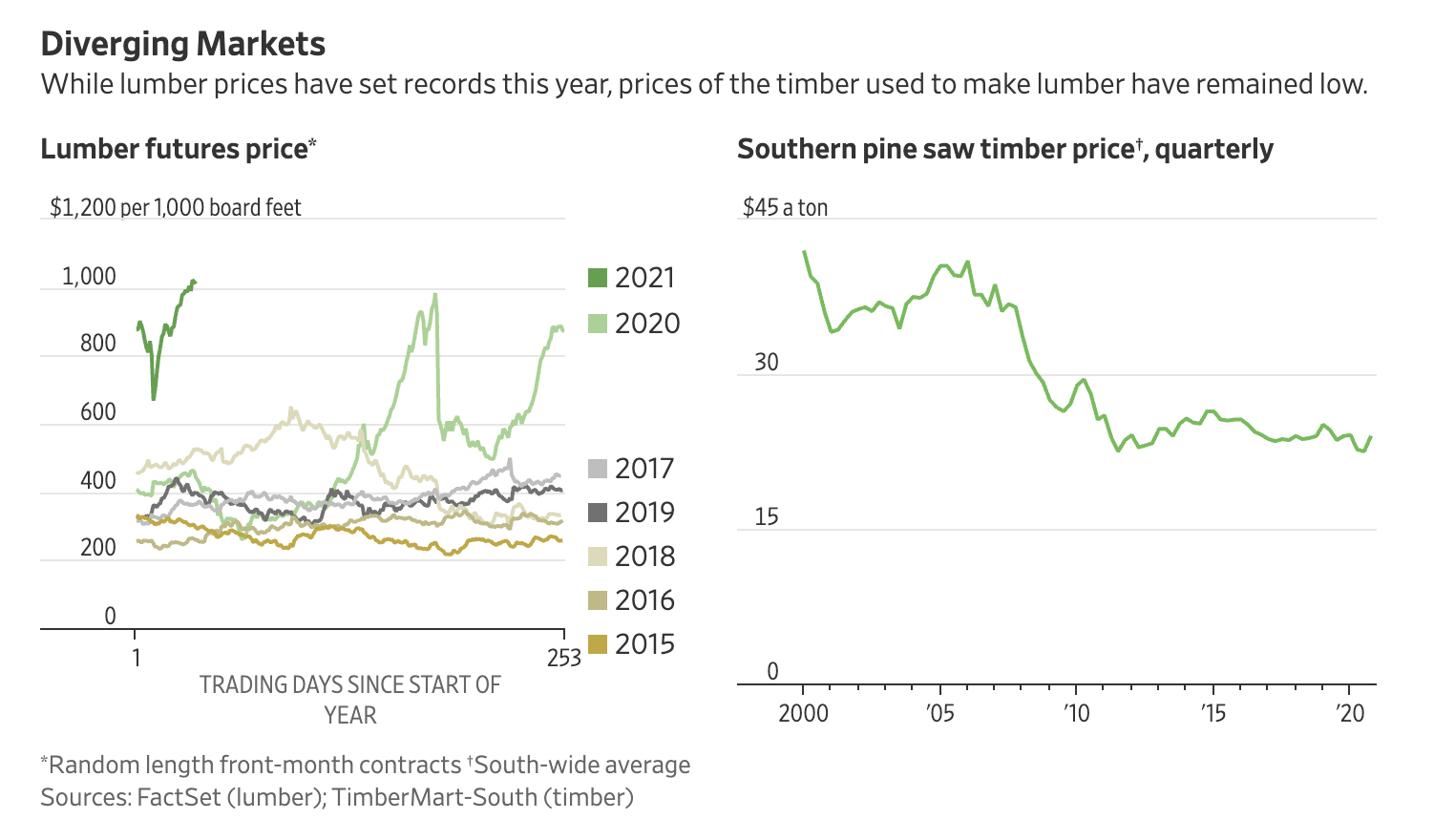

Chart of the Day:

From the excellent Wall Street Journal piece Lumber Prices Are Soaring. Why Are Tree Growers Miserable? (NRB)

Quick Links:

Tom Vanderbilt sent over this excellent 2016 piece on DIY YouTube he wrote after yesterday’s edition. (NRB)

Jill Lepore’s New Yorker review of Nicole Perlroth’s new book This Is How They Tell Me the World Ends.(NRB)

Thanks for reading,

Noah (NRB) & Colin (CJN) & Guan (GY)

—

Why is this interesting? is a daily email from Noah Brier & Colin Nagy (and friends!) about interesting things. If you’ve enjoyed this edition, please consider forwarding it to a friend. If you’re reading it for the first time, consider subscribing (it’s free!).